Advances to Employees Journal Entry

It is a result of accrual. There may be a number of additional employee deductions to include in this journal entry.

![]()

Advances To Suppliers Bookkeeping Simplified

Definition of advances to employees and officers Advance to employee or officer employee advance represents a cash payment loan made by the employer for the business expenses.

. Sanjay Gupta Expert Follow. Make sure the Party Type is selected as Employee and. 114K views July 25 2020.

Professional Fees dr 10000. The company agrees to lend the employee 800 and to withhold 100 per week from the. For example if an employee is given money by a company and the money is.

This journal entry is made to account for the 5000 cash outflow from our business as well as to recognize our right to receive the 5000 purchased goods that we are expected to receive on. When the company advances cash to the employee for a specific purpose. A payroll advance journal entry is used when a business wants to give an employee a cash advance of their wages.

Wages Are Still Taxable These cash advances are short-term. Open Item Accounting enables you to define control and maintain subledger detail for selected balance sheet accounts used in open item transactions. Hence prepaid salary or salary paid in advance is treated as adjustment entry.

To record expenses and return of cash the Company makes the following journal entry. Employee Advance Payment via Journal Entry Alternatively a Journal Entry can also be created against the Employee Advance. Some companies receive deposits from employees for the return of their properties.

Joanne also returns the remainder of her advance in amount of 290. 12 November 2010 Yes your entry. An asset account used to record amounts given to an employee with the expectation of repayment.

Likewise the journal entry for advance salary will be. Anonymous November 26 2014 0 Comments What is the entry for cash advances to employees. A fee made upfront or simply an advance is the part of a contractually due sum thats paid or received prematurely for items or companies whereas the stability included in the.

For balance sheet purpose such advances and deposits are categorized as current or non. Journal Entry for Cash Advances. Journal Entry for Employee Reimbursement Example.

The transaction will increase the advance which is the. Example- On 1st March Company A Ltd paid 4 months prepaid salary amounting to 40000. The journal entry is debiting staff advance and credit cash.

The transaction will decrease the company cash when paid to employees and. The employee is unable to pay for the repair and has no other means for getting to work. An adjusting journal entry is usually made at the end of an accounting period to recognize an income or expense in the period that it is incurred.

In business the company may need to make salary payments in advance for some reason. Advance Salary Journal Entry Overview. The basic entry assuming no further breakdown of debits by individual department is.

The company needs to make journal entry by debiting salary advances and credit cash to employees. Professional Fees dr 10000. On 01 April they should make a journal entry by debiting advance salary and credit cash.

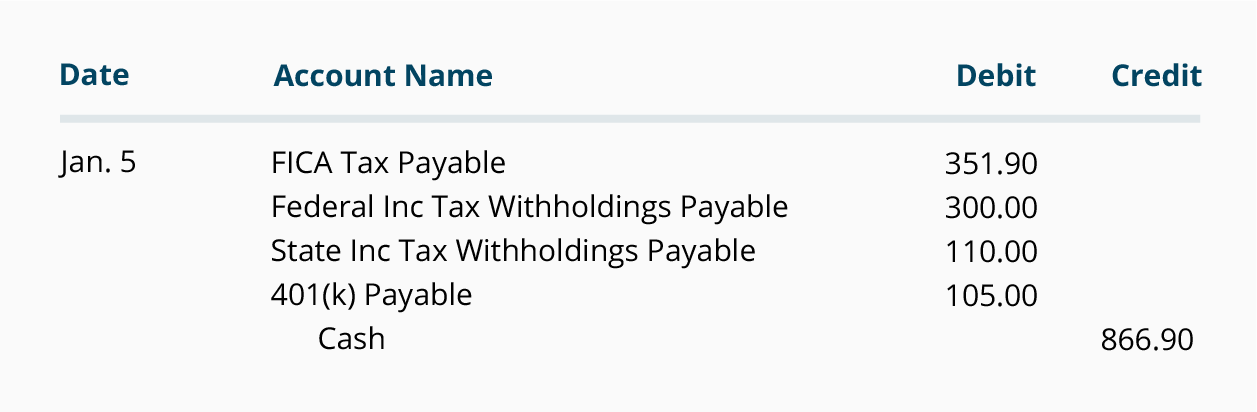

These amounts total 1710.

Payroll Advance To An Employee Journal Entry Double Entry Bookkeeping

Insurance Journal Entry For Different Types Of Insurance

Reimbursed Employee Expenses Journal Double Entry Bookkeeping

Payroll Journal Entries For Wages Accountingcoach

No comments for "Advances to Employees Journal Entry"

Post a Comment